What is PAYE (Pay As You Earn)?

PAYE stands for Pay-As-You-Earn. It is the method of collecting Income Tax from employees on their earnings. Under this system, an employer is required by law to deduct income tax from an employee’s taxable salary or wages. It could be weekly, fortnightly or monthly hence the name Pay As You Earn.

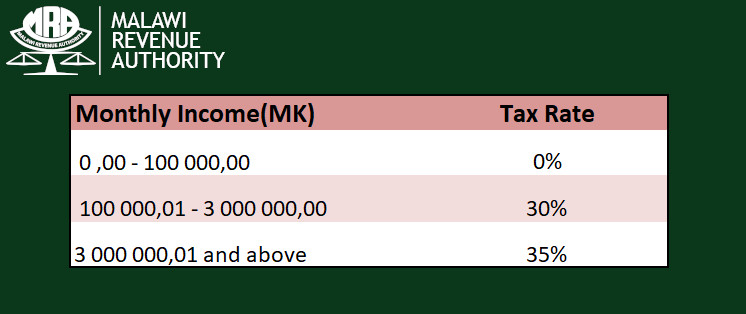

PAYE Calculation Slab

PAYE income tax calculation is based on the tax slab split income wise. It’s a progressive slab system. Employees with higher wages are obliged to pay more than the employees who earn less. The total taxable income of employee is split in brackets as defined in the slab (0-100 000,00 | 100 000,01-3 000 000,00 etc). Amount applicable in each tax bracket attracts the corresponding percentage of tax and the total is summed at last the tax liable. The Malawi Revenue Authority has announced that the Taxation (Amendment) Act has been gazetted. The Eleventh Schedule to the Taxation Act has the following amended tax table for PAYE:

Calculation of PAYE

Advantages of PAYE to taxpayers

- It is convenient to pay while the money is available.

- It is easy and cost effective to pay.

- Affords the taxpayer to pay by instalments other than having the burden to pay a lump sum.

Withholding Tax

The Taxation Act, Fourteenth Schedule, has been amended as follows;

– Introduced 20% Withholding Tax on winnings on betting and gambling transactions including lotteries. Winnings means any payment made to any person who wins a bet or a gamble including a lottery.

– Increased tax-free threshold for casual labour from K15,000 to K35,000 per transaction.

– Payment in excess of K35,000 for casual labour charged at 20%.

– Increased Withholding Tax on rent from 15% to 20%. Rent includes rent for movable and immovable property whether paid under a lease or otherwise but excludes rent payable by an individual whose source of income is only from employment and the rent is payable in respect of property used as a dwelling house.

– Increased Withholding Tax on fees from 10% to 20%.

– Introduced 3% Withholding tax on payment for farm produce other than tobacco

Other Amendments to the Taxation Act

The Taxation Act, Section 2, has been amended on the definition of the words “amount realized” by deleting paragraph (a) and substituting it with the following new paragraph (a); “in the case of disposal of an asset by sale for cash, means the cash received or contracted to be received, including any contingent amount agreed at the time of disposal”.

The Taxation Act, Section 15 (1) paragraph (e) has been amended by inserting immediately after the word “trust” the words “in which the individual is a settler of a trust”.

Value Added Tax(VAT)

The VAT Act has been amended in order to introduce a 16.5% VAT on refined cooking oil.

FORM 12 For PAYE Returns

The Malawi Revenue Authority (MRA) has introduced a new and simplified Form 12 for Pay As You Earn (PAYE).

Leave A Comment

You must be logged in to post a comment.