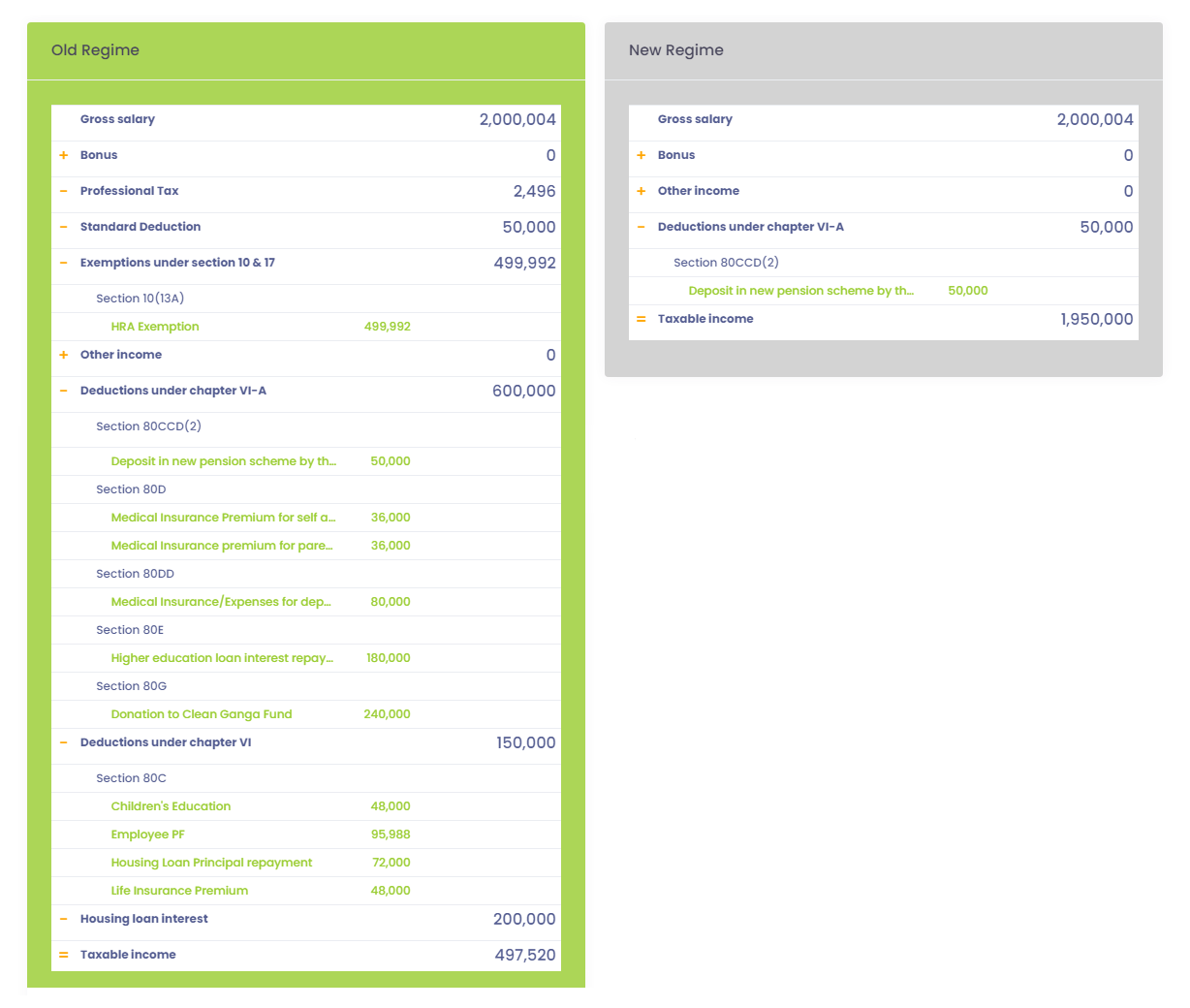

The new Budget for the financial year 2020-21 introduced a new income tax regime for individual taxpayers. However, the new tax regime requires the individual taxpayer to renounce certain specified deductions. Under the new income tax regime, taxpayers cannot claim the standard deduction of Rs. 50000, no deductions based on section 80C, interest on the self-occupied property of Rs. 2 lakhs, and other deductions which are availed by many taxpayers. In fact, the new tax regime allows the taxpayers to claim only one deduction – which is section 80 CCD(2). Section 80CCD (2) allows salaried individuals to claim deductions up to 10% of their salary which includes the basic pay and dearness allowance or is equal to the contributions made by the employer towards the NPS.

From April 1, 2020, an individual taxpayer will have the option either to continue with the existing tax regime or opt for the new tax regime without 70 tax exemptions and deductions. Salaried individuals, having no business income, can choose between the existing and new tax regimes every financial year, as per their convenience. In order to know which tax regime is beneficial for an individual, it is important to know how much will be the tax liability in both regimes.

Comparison of Old and New tax regimes

The most important point that the comparison between the new and old tax regime highlights is the fact that the new budget tries to curtail the option to save the incentives and puts more money in the hands of taxpayers. Taxpayers who have maintained their financial portfolio to avail tax deductions as per the old slab are likely to pay more tax under the new tax slabs.

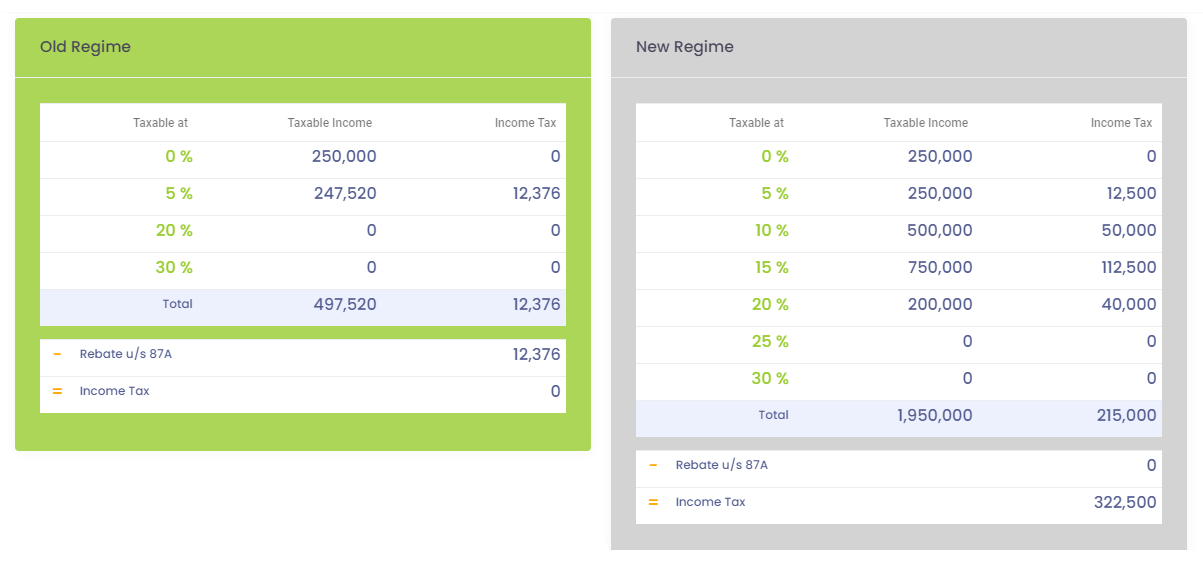

So, coming to the old tax rates- it was nil for the annual income up to Rs. 2.5 lakhs, 5% for annual income between Rs. 2.5 lakhs to Rs. 5 lakhs. 10% for income group between Rs. 5 lakh and Rs. 12.5 lakh and 30% for Rs. 12.5 lakh and above.

In the new tax regime, the income group between Rs. 5 lakhs and Rs. 7.5 lakhs would be required to pay income tax at 10%. And the income group ranging from Rs. 7.5 lakhs to Rs. 10 lakh will be required to pay tax at 15%. Those falling in the income group of Rs. 10-12.5 lakhs and Rs. 12.5-15 lakhs will be levied tax at 20% and 25% respectively. It is seen that the new tax regime is likely to make taxpayers pay a higher tax amount in the long-term in comparison to the old regime.

In the old tax regime, the taxpayers benefitted from several tax exemptions and deductions including tax deductions on health insurance and Equity-linked savings schemes investments under section 80 C like LIC and house rent allowance, which is not possible on switching to the new system because the new tax policy does not offer exemptions like the old one. In simple words, a salaried taxpayer will have to forgo the available deductions and exemptions in the old tax regime if he wishes to switch to the new tax regime.

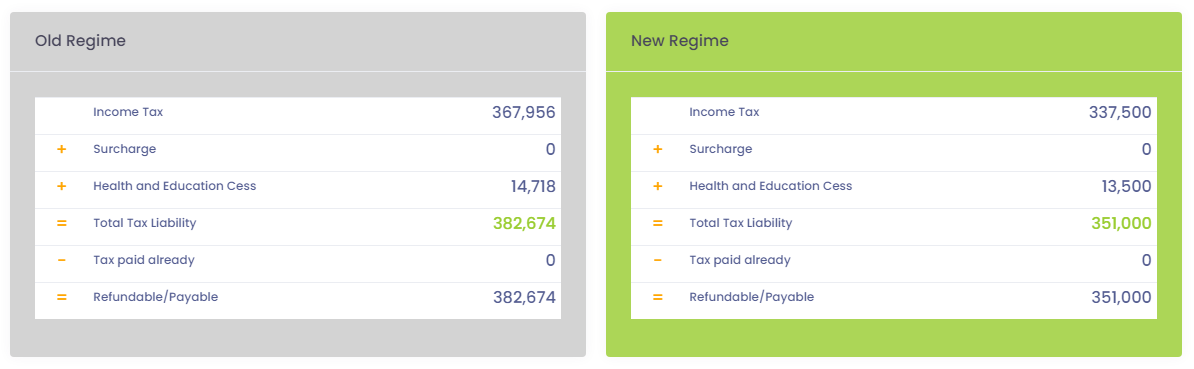

Another important point is that the surcharges still remain the same with the new tax regime. Surcharge rates are same as it was with the old tax regime. Both regimes charge a surcharge of 10% for taxpayers who fall in Rs. 50 lakhs to Rs. 1 crore bracket, 15% for those in Rs. 1 crore to 2 crores rupees, 25% for Rs. 2 crores to Rs. 5 crores category, and finally 37% for who claim income that is over and above Rs. 5 crores.

Health and Education cess at the rate of 4 per cent will be added to the Income Tax liability in all the cases.

| Annual Income (Rs.) | Old Tax Rate | New Tax Rate |

|---|---|---|

| Up to Rs. 2.5 lakhs | Nil | Nil |

| Rs. 2.5 lakhs to Rs. 5 lakhs | 5% | 5% |

| Rs. 5 lakhs to Rs. 7.5 lakhs | 20% | 10% |

| Rs. 7.5 lakhs to Rs. 10 lakhs | 20% | 15% |

| Rs. 10 lakhs to Rs. 12.5 lakhs | 30% | 20% |

| Rs. 12.5 lakhs to Rs. 15 lakhs | 30% | 25% |

| Rs. 15 lakhs and above | 30% | 30% |

Things to consider:

• The above-mentioned new tax regime rates are without any deductions under different sections of Chapter VI-A.

• If a taxpayer claims a deduction of Rs. 2.5 lakhs (standard deduction of Rs. 50,000, Rs. 1.5 lakhs u/s 80C, and investment in NPS of Rs. 50,000), the tax will remain the same as the old one.

• In case he also claims home loan interest deduction of Rs. 2 lakhs or HRA exemption, the old tax slab rate would be Rs. 46,800 lesser than the new regime.

Comparison of Old and New tax regimes for taxpayers at different income levels

The new and old tax regimes can be understood better if we compare taxpayers of different income levels and the tax liability derived from both regimes.

Individual Income Rs. 10 lakhs, living in own house so does not claim HRA and is under 60 years of age group.

| Old Slabs | Old Tax Rates (in Rs.) | New Slabs | New Tax Rates (in Rs.) | |

|---|---|---|---|---|

| Income | 10,00,000 | 10,00,000 | ||

| Deductions 80C | 150,000 | N/A | ||

| Deductions 80D | 25,000 | N/A | ||

| House Loan | 200,000 | N/A | ||

| Standard Deduction | 50,000 | N/A | ||

| Taxable Income | 5,75,000 | 10,00,000 | ||

| Slabs | 2.5-5 lakhs at 5% +5-7.5 lakhs at 20% | 12500+15000 | Rs. 2.5-5 lakhs at 5% +Rs. 5-7.5 lakhs at 10%+Rs. 7.5-10 lakhs | 12500+25000+.37,500 |

| Total tax payable as per the income tax slab | 27,500 | 75,000 |

Now let’s see how the income group above Rs. 15 lakhs will be charged in the old regime and the new regime. This is a separate calculation from the above table:

Income: Rs. 15 lakhs

| Old Regime with Deductions (in Rs.) | Old Regime without Deductions (in Rs.) | New Regime (in Rs.) | |

|---|---|---|---|

| Income | 15 lakhs | 15 lakhs | 15 lakhs |

| Exemptions/Deductions | 2 lakh (Rs. 1.5 lakhs u/s 80C + Rs. 50,000 standard deduction) | Nil | Nil |

| Taxable Income | 13 lakhs | 15 lakhs | 15 lakhs |

| Total Tax | 202,500 | 262,500 | 187,500 |

Income: Rs. 30 lakhs

| Old Regime with Deductions (in Rs.) | Old Regime without Deductions (in Rs.) | New Regime (in Rs.) | |

|---|---|---|---|

| Income | 30 lakhs | 30 lakhs | 30 lakhs |

| Exemptions/Deductions | 425000 | Nil | Nil |

| Taxable Income | 25,75,000 | 30,00,000 | 30,00,000 |

| Total Tax | 585,000 | 712,500 | 637,500 |

The above payable tax would include Cess @ 4% extra. The above calculation is for reference purposes only.

* Deductions Applicable: Rs 1.5 lakhs u/s 80C; Rs. 50,000 standard deduction; Rs.25,000 u/s 80D; Rs. 2 lakhs home loan interest u/s 24.

Income: Rs. 60 lakhs

| Old Tax Rate with Deductions (in Rs.) | Old Tax Rate without Deductions (in Rs.) | New Regime (in Rs.) | |

|---|---|---|---|

| Income | 60 lakhs | 60 lakhs | 60 lakhs |

| Exemptions/Deductions | 425,000 | Nil | Nil |

| Taxable Income | 55,75,000 | 60,00,000 | 60,00,000 |

| Surcharge @ 10% | 1,48,500 | 161,250 | 1,53,750 |

| Total Tax | 16,33,500 | 17,73,750 | 16,91,250 |

* Deductions Applicable: Rs 1.5 lakhs u/s 80C; Rs. 50,000 standard deduction; Rs.25,000 u/s 80D; Rs. 2 lakhs home loan interest u/s 24.

Comparison of Exemptions and Deductions in the old and new tax regimes

The Old tax regime allows many exemptions and deductions whereas the New tax regime allows just a few exemptions and deductions

Comparison of Tax Slabs in the old and new tax regimes

The Old Regime has different tax slabs according to the age of the employee, but, the New Regime has a fixed tax slab for all age groups

Comparison of Tax Liability in the old and new tax regimes

Tax Liability is calculated the same way in both Old and New tax regimes.

Leave A Comment

You must be logged in to post a comment.